How to Read and Interpret Balance Sheets Fast

The balance sheet, also known as the Statement of Financial Position, is one of the three key financial statements. For every business, whether it is big or small, it is an utterly essential component.

FINANCE

Dezmon

11/27/20256 min read

The balance sheet, also known as the Statement of Financial Position, is one of the three key financial statements. For every business, whether it is big or small, it is an utterly essential component. By looking at its three main elements — assets, liabilities, and equity — it gives them an overview of the company’s financial situation at a specific point in time. Therefore, entrepreneurs can assess the potential risks and make a suitable decision for the business. This article will equip them with the knowledge on how to make use of the balance sheet effectively.

Balance Sheets Three Main Elements

To give you a better understanding of its concept, let’s have a look at the following example. A company takes out a loan worth $10,000 from a bank. The amount will be recorded both in the total assets of the company as cash, and in the total liabilities as short- or long-term debt, balancing the equation.

On the other hand, if the company is given a $20,000 sum of funds by its investors, the amount will be recorded in the total assets as cash and as share capital in the total equity section. When the company generates revenue in excess of its expenses, the profit will go into total equity as retained earnings and at the same time, as either cash or receivables (owed money) in the total assets.

With this method of balancing values, a company can remain sure that the recorded values are correct and reduce the risk of making mistakes and errors in their accounts.

Balance Sheet Concept Example

To give you a better understanding of its concept, let’s have a look at the following example. A company takes out a loan worth $10,000 from a bank. The amount will be recorded both in the total assets of the company as cash, and in the total liabilities as short- or long-term debt, balancing the equation.

On the other hand, if the company is given a $20,000 sum of funds by its investors, the amount will be recorded in the total assets as cash and as share capital in the total equity section. When the company generates revenue in excess of its expenses, the profit will go into total equity as retained earnings and at the same time, as either cash or receivables (owed money) in the total assets.

With this method of balancing values, a company can remain sure that the recorded values are correct and reduce the risk of making mistakes and errors in their accounts.

Common Balance Sheet Items

Elements of the balance sheet can vary from industry to industry. However, there are common items that can be found in every balance sheet. For solopreneurs and small businesses, their balance sheet might include the following components.

Assets: One of the three variables in the formula. Like how it is mentioned before, this is where the items that bring benefits/revenue to the company are included. The assets can be further divided into current and noncurrent assets, based on its liquidity:

1. Current Assets: are assets which can be turned into cash in less than one fiscal year, which includes:

Cash and Equivalents: The most liquid of all assets. On-hand cash and bank savings are included in this item. Other items which have a maturity of one fiscal year or less are sometimes lumped under this category as well.

Account receivable (AR): This represents the credit that is owed to the company. For instance, the payment which has not been collected from a customer.

Inventory: It refers to all raw materials, unfinished products, and goods available for sale of the company. This account directly relates to the income statement as it is used to calculate the cost of goods sold (COGS).

Prepaid expenses: They are the expenses that the company has paid for in advance (and is expected to bring benefits/revenue to the company), such as insurance premiums, advertising bundles, or rent payments.

2. Noncurrent Assets: are assets which cannot be readily turned into cash within a fiscal year. For small businesses and solopreneurs, these may include:

Long-term Investments: the amount of investments made in other assets that cannot be liquidated within one fiscal year.

Plant, Property, and Equipment (PP&E): also known as Fixed Assets or Tangible Assets, are assets which are expected to generate value to the company over a long period of time. They are usually associated with depreciation expenses in the income statement.

Intangible Assets: involve assets that are similar to PP&E, but are non-physical, such as licenses and patents. They are often involved with amortization expenses in the income statement.

Liabilities are debts or burdens that a company has to pay back to the relevant parties. Similar to the assets, liabilities can be divided into current and noncurrent liabilities:

1. Current Liabilities: refer to liabilities that are due within one fiscal year. This includes:

Accounts Payable (AP): the amount of credit owed by the company to other parties, such as money owed to suppliers from the purchase of products and materials.

Current Debts: refers to debts incurred from cash or fund borrowings which are due within one fiscal year, a lot of times it is referred to as Note Payables.

Current Portion of Long-term Debts: the portion of the long-term debt obligations that is due within the current fiscal year.

2. Noncurrent Liabilities: represent debts that are due after one fiscal year. For small businesses and solopreneurs, this account will mainly display Long-term Debts, which are usually funds borrowed from banks.

Shareholders’ equity is the last variable in the balance sheet. This where the items related to the capital of the company are listed. For small businesses, they should consist of two items:

Share Capital: is the amount of capital invested in the company by its owner or shareholders. It represents how much of the company’s total value that can be claimed by its shareholder, after deducting the debts. This item can go by many names, such as Common Stock, Owner’s Capital, Capital Stock, etc.

Retained Earnings: just as its name suggests, these are the profits retained by the company after deducting all related expenses and dividends from them.

Balance Sheet Analysis

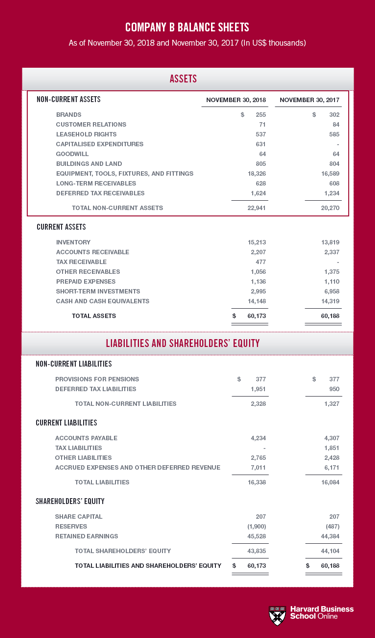

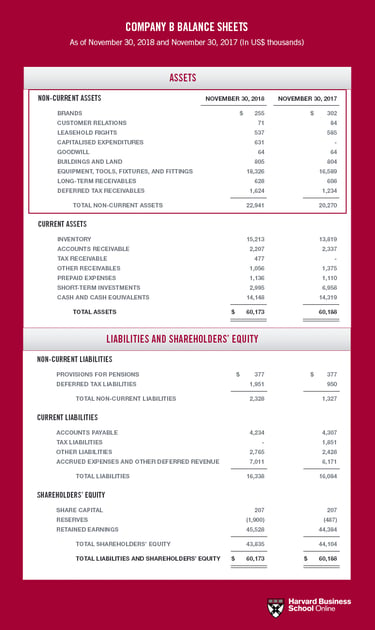

Like other statements, there are many ways to analyze a balance sheet. One can use it to test the company’s financial strength, liquidity or compare its performance with its own historical values or a competitors’. Here’s an example from Harvard Business School, comparing a balance sheet of Company B between year 2017 and 2018:

Before diving into the details, you should take a look at the top of the balance sheet first. The name of the company, date issued and most importantly, the units will be shown here. This is a very important step as different companies sometimes use different formats and units.

Let’s start off by looking at the proportion of Company B’s debt and equity in 2017. From the given information, you can see that most of the capital Company B owns came from its equity, with the exact amount being $44.1M in contrast to its $17.4M in debts. This means that around 72% of the company’s funds are from its equity. The situation is similar in 2018, where the proportion of the equity is at 70%

References:

https://www.investopedia.com/terms/f/financial-statements.asp

https://corporatefinanceinstitute.com/resources/knowledge/accounting/balance-sheet/

https://corporatefinanceinstitute.com/resources/knowledge/finance/marketable-securities/

https://www.investopedia.com/terms/m/marketablesecurities.asp

https://corporatefinanceinstitute.com/resources/knowledge/accounting/what-is-accounts-receivable/

This shows a very healthy financial situation for the company. Think of it this way: if the company were to suddenly stop all of its operation and all its debtors want to take their money back, the company will be able to afford all the debt repayment obligations.

Now, we move on to the Assets. The main issue we should try to observe here is the company’s liquidity. In 2017, we can see that out of $60.2M in total asset value, around $40M is from current assets which mostly consists of Inventory and Cash. On the other hand, noncurrent assets valued at $20.2M, mostly from Equipments. The situation is nearly the same in 2018.

Once again, Company B shows a good situation, this time in terms of liquidity due to its high proportion of current assets that can be readily liquidated into cash in a short amount of time.

For Liabilities and Equity, the only thing worth noticing here is the increase in Retained Earnings between 2017 and 2018, which indicates a profitable year in 2017. Like how it is mentioned before, the amount of liabilities that the company owned is very small. This means that the company has room for growth through the issuance of more debts.

Overall, one could say that Company B is an ideal company many would want to have. It has good financial strength, good liquidity and it also generates good profit each year.

Copyright © 2025 Dezmon Landers