Getting Into The Details of Cash Flow Statements

The cash flow statement (CFS) is one of the three key financial statements.

FINANCE

Dezmon

11/27/20254 min read

The cash flow statement is one of the three key financial statements of a company. It is the bridge between the income statement and the balance sheet, showing the amount of cash and equivalents coming in and out of a business during a specific fiscal period.

The statement represents a business’s capacity for cash generation and the level of liquidity. In other words, it measures whether the company is able to 1) pay its debts on time, 2) support its operating costs, and 3) have leftover cash for additional investments.

Since this statement’s concept revolves around cash inflows and outflows of the company, an increase in value for items in this statement indicates cash inflows, while an item with decreased value represents cash outflows. This article will take you through the structure of the cash flow statement, its concepts, and how to use them to analyze a company’s cash management.

The Structure Of Cash Flow Statement

Cash Flow From Operating Activities

This type of cash flow typically includes all sources and usages of cash from business operations, mainly related to current assets and current liabilities. For example, the receipts from sales of products and services, interest payments, income tax payments, supplier-related payments, employment, rent payments, etc.

Cash Flow From Investing Activities

This section involves any cash flows related to the acquisition and disposal of long-term assets. These investing activities may include purchases or sales of property, plant, and equipment (PP&E), long-term investments, etc. Most of the time, transactions found in this category are cash-out items since it is more common to purchase/invest in new long-term assets than selling them off.

Cash Flow From Financing Activities

This category covers cash flows received from or paid to shareholders and debtors. For example, dividend payments, loan repayments, or stock repurchases. However, it should be noted that interest paid is categorized as an operating activity since it is considered as the cost of borrowing money, which allows the company to continue its operations.

Preparing the cash flow statement

The cash flow statement can be prepared using two different methods: direct and indirect methods. The difference lies in the calculation of cash flows from operating activities. For investing and financing sections, presenting directly or indirectly leads to the same result. Most companies opt to implement the indirect method since it is easier and takes less time to prepare. Below is the explanation and examples of both methods.

Direct Cash Flow Method

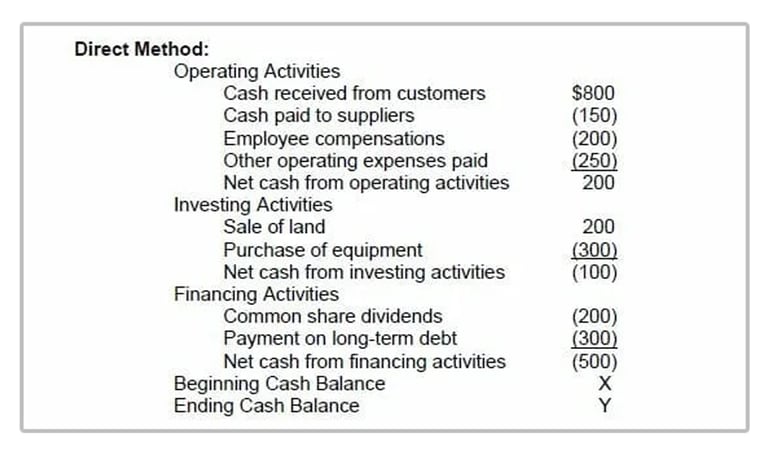

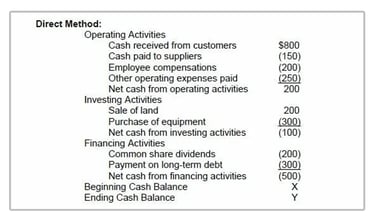

This method is more suitable for small businesses and solopreneurs since their statement items are less complex. The direct method calculates the company’s remaining cash flow by taking into account all cash payment and receipt activities during its operations, before calculating them together with the cash flows from investing and financing activities. The result is then added to/subtracted from the initial cash balance of the period.

Simply put, all cash-related items are lined up and the resulting sum is added to/deducted from the beginning cash balance of the period in order to arrive at the ending balance. You can see an example case of this from the picture below:

Indirect Cash Flow Method

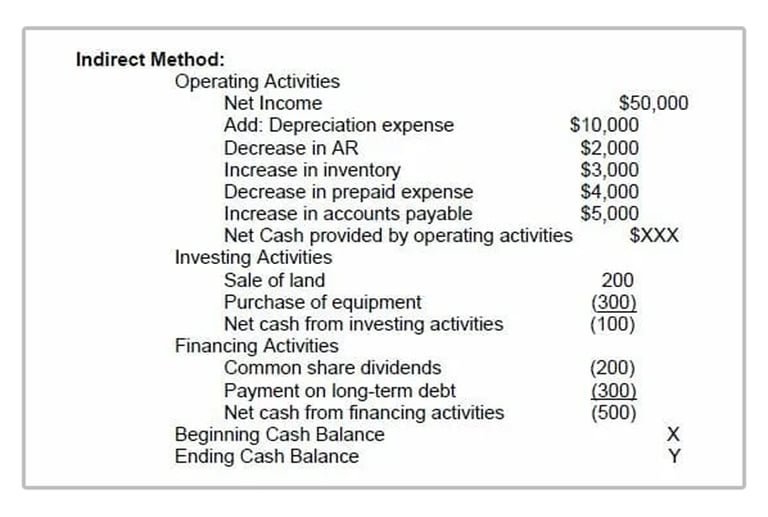

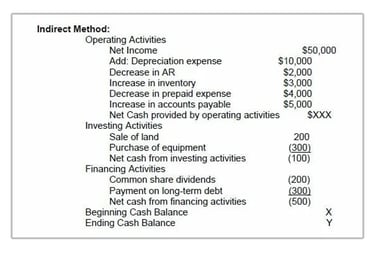

The indirect method, on the other hand, utilizes the data from the income statement to help with the calculation. The calculation starts with net income (or net loss) from the income statement. The figure is then modified by adding in non-cash expenses, liquidation of current assets and acquisition of debts, while deducting cash expenses, increase in current assets and repayment of debts. The result is then calculated with the figures from investing and financing activities, and finally added to/deduct from the beginning cash balance.

The logic behind this method is to reverse-engineer the figure from Net Income back to Cash and Equivalents by deducting cash-paying items out and adding cash-receiving items in. As mentioned before, this method is more commonly used, especially in big companies, due to its simplicity in statement preparation. You can see the calculation from the picture below:

Conclusion

In the business world, profit isn’t always the most important variable. Having adequate cash and liquidity is also very important. A company cannot continue to invest and improve its growth without having cash on hand, and a company that cannot grow is considered dead or at the verge of being so.

The cash flow statement is an essential tool that can be used to measure the company’s cash availability or liquidity in each fiscal period, while showing the amount of cash that is being spent in important activities like investments.

However, negative cash flow does not necessarily mean a bad thing. Sometimes, it displays an attempt to expand its business at a particular time, which might denote a promising outlook for a company. Nevertheless, it is a good idea for entrepreneurs to frequently examine the cash flow statement in order to gain a better understanding of the company performance.

Copyright © 2025 Dezmon Landers